: Empowering India’s Micro and Small Entrepreneurs")

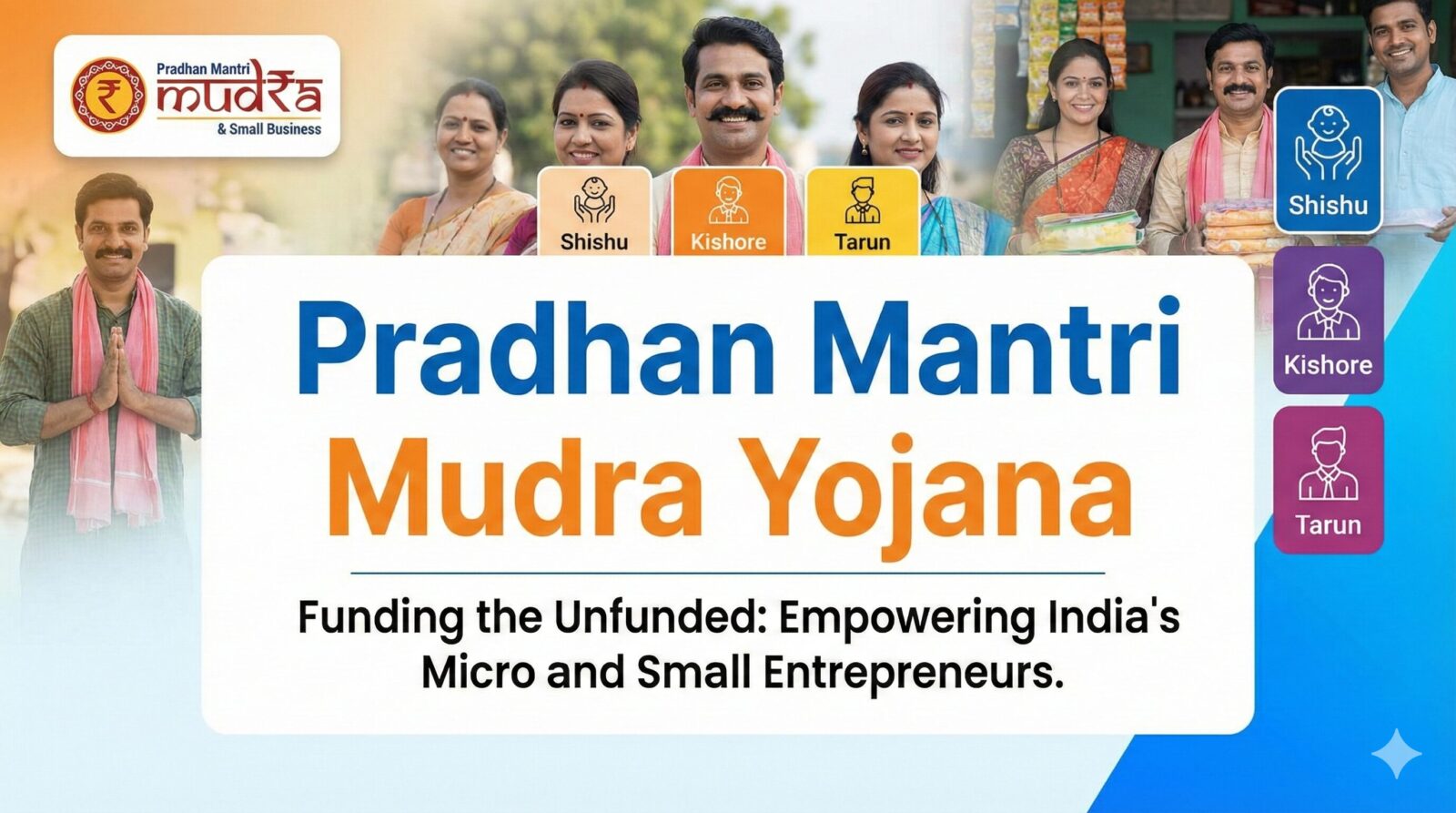

The economic backbone of India is its micro, small, and medium enterprises (MSMEs), which play a pivotal role in employment generation, innovation, and overall economic development. Recognizing the significance of small businesses, the Government of India launched the Pradhan Mantri MUDRA Yojana (PMMY) on April 8, 2015 under the leadership of the Hon’ble Prime Minister. Pradhan Mantri MUDRA Yojana. The scheme was designed to provide financial support to the non-corporate, non-farm sector entrepreneurs, enabling them to expand their businesses, improve livelihoods, and contribute more substantially to India’s economy.

Through PMMY, entrepreneurs can avail loans categorized under the MUDRA loan framework, with financial institutions providing funding up to ₹20 lakh for those who have previously availed and successfully repaid loans under the ‘Tarun’ category. Pradhan Mantri MUDRA Yojana. These loans aim to bridge the credit gap for small and micro enterprises and provide them a growth trajectory aligned with their developmental stages.

Understanding the Core Objective of PMMY

The primary objective of the Pradhan Mantri MUDRA Yojana is to empower small entrepreneurs by giving them easy access to financial resources. Many small business owners in India often face challenges in securing loans from formal financial institutions due to lack of collateral, limited credit history, or small scale of operations. PMMY addresses this gap by offering collateral-free loans through a wide network of financial institutions, ensuring that access to credit is not a barrier to entrepreneurial growth.

Some of the key aims of the scheme include:

- Promoting entrepreneurship among micro and small business owners.

- Increasing access to institutional credit for non-farm, non-corporate enterprises.

- Supporting livelihood generation and promoting self-employment opportunities.

- Encouraging graduation and scaling up of small businesses from micro to medium enterprises.

By addressing the financial constraints of small business owners, PMMY strengthens India’s entrepreneurial ecosystem while simultaneously contributing to job creation and economic stability.

Who Can Benefit from PMMY?

PMMY specifically targets non-corporate, non-farm small and micro enterprises. These are businesses that operate at a small scale, often run by individual entrepreneurs, partnerships, or proprietorships. Some examples include:

- Local retail shops

- Small manufacturing units

- Service-based businesses like salons, repair shops, or logistics services

- Street vendors and small traders

- Handicraft and cottage industries

Essentially, the scheme is inclusive, catering to both first-time entrepreneurs as well as those who have already received support under earlier MUDRA loans.

Eligibility Criteria

To avail PMMY loans, applicants must meet the following criteria:

- Be engaged in a non-corporate, non-farm business activity.

- Operate as a small or micro enterprise, as defined by the government.

- For higher-tier loans (up to ₹20 lakh), the applicant should have successfully repaid previous loans under the ‘Tarun’ category.

- Approaching any of the participating lending institutions such as Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks, Microfinance Institutions (MFIs), or Non-Banking Financial Companies (NBFCs).

This wide eligibility ensures that the benefits of PMMY reach a large and diverse group of entrepreneurs, including those from underprivileged backgrounds.

MUDRA Loans: The Heart of PMMY

Under PMMY, loans are classified as MUDRA loans, each designed to cater to businesses at different stages of growth. MUDRA has created four distinct products to guide and support entrepreneurs through their business journey:

1. Shishu – The Starting Point

- Loan Amount: Up to ₹50,000

- Target: Businesses in the initial stage of operations

- Purpose: To provide seed capital for micro-enterprises to start or stabilize operations

- Example: A person opening a small street food stall or tailoring unit

Shishu loans are ideal for first-time entrepreneurs who require small amounts to initiate their business and establish cash flow.

2. Kishore – The Growth Stage

- Loan Amount: ₹50,001 to ₹5,00,000

- Target: Businesses in the early growth phase

- Purpose: To expand operations, purchase machinery, or increase working capital

- Example: Expanding a local grocery store into a chain of stores

Kishore loans encourage businesses to scale up after they have established their initial operations, allowing them to enhance productivity and generate higher revenue.

3. Tarun – The Expansion Phase

- Loan Amount: ₹5,00,001 to ₹10,00,000

- Target: Established businesses seeking further expansion

- Purpose: To fund significant business activities, such as adding production lines or entering new markets

- Example: Upgrading a small manufacturing unit to a medium-scale production facility

The Tarun category supports businesses ready to graduate from small to medium enterprises, emphasizing sustainable growth and long-term success.

4. TarunPlus – Advanced Scaling

- Loan Amount: Up to ₹20,00,000

- Target: Successful entrepreneurs who have repaid previous loans

- Purpose: To provide funding for large-scale expansion, modernizing operations, or entering new business sectors

- Example: Opening multiple branches of an established chain or investing in advanced technology for production

TarunPlus loans are intended for seasoned entrepreneurs looking to take their business to the next level, ensuring continuity and long-term growth.

How to Apply for PMMY

PMMY loans are accessible through multiple channels, making the application process simple and convenient. Entrepreneurs can approach any of the participating financial institutions:

- Commercial Banks

- Regional Rural Banks (RRBs)

- Small Finance Banks

- Microfinance Institutions (MFIs)

- Non-Banking Financial Companies (NBFCs)

Online Application

In addition to visiting the bank or institution physically, applicants can also apply online through the government portal. The online platform is user-friendly and allows applicants to:

- Fill out the application form

- Upload required documents

- Track loan application status

- Receive guidance on loan categories and eligibility

This digital interface has made PMMY accessible to a larger audience, including entrepreneurs in remote and rural areas.

Advantages of PMMY for Entrepreneurs

PMMY offers multiple benefits to micro and small business owners:

- Collateral-Free Loans: Eliminates the need for security deposits, reducing barriers for small entrepreneurs.

- Flexible Loan Categories: From Shishu to TarunPlus, the loans are tailored to the growth stage of the business.

- Wide Accessibility: Available through banks, NBFCs, MFIs, and online portals, ensuring maximum reach.

- Support for Business Growth: Loans can be used for working capital, equipment purchase, business expansion, and more.

- Empowerment of Non-Corporate Entrepreneurs: Helps small traders, artisans, and service providers access formal credit.

- Promotes Financial Inclusion: Encourages the adoption of formal banking systems among small-scale entrepreneurs.

Overall, PMMY is not just about lending money; it is about empowering entrepreneurs to grow sustainably and contribute meaningfully to the economy.

The Economic Impact of PMMY

Since its inception in 2015, PMMY has had a profound impact on India’s economic landscape:

- Job Creation: By supporting small businesses, PMMY indirectly generates employment opportunities in local communities.

- Boosting Entrepreneurship: Many first-time business owners have turned their ideas into sustainable enterprises with PMMY loans.

- Strengthening the MSME Sector: MSMEs account for a significant portion of India’s GDP. Financial support through PMMY ensures these units can compete, innovate, and grow.

- Promoting Financial Literacy: Entrepreneurs learn to navigate formal banking systems and manage credit responsibly.

The scheme has proven particularly transformative for women entrepreneurs and rural businesses, who often face challenges in accessing conventional bank loans.

Challenges and Areas for Improvement

While PMMY has been widely successful, certain challenges remain:

- Awareness Gaps: Many potential beneficiaries are unaware of the scheme or its online application process.

- Documentation Issues: Small entrepreneurs sometimes struggle with the paperwork required to secure loans.

- Loan Disbursement Delays: Banks and NBFCs occasionally take longer than expected to process applications.

- Financial Literacy Needs: Some entrepreneurs require guidance in managing loans and planning repayments.

Addressing these challenges could further enhance the scheme’s reach and impact, ensuring that more micro and small enterprises benefit from government support.

PMMY and the Vision for India’s Future

The Pradhan Mantri MUDRA Yojana aligns closely with India’s vision of inclusive economic growth and self-reliant entrepreneurship. By providing structured, accessible credit, the government empowers individuals to pursue business opportunities, generate employment, and strengthen the local economy.

Through its tiered loan structure—Shishu, Kishore, Tarun, and TarunPlus—PMMY also creates a clear roadmap for business growth. Entrepreneurs are not just given funds; they are offered a path to scale their operations responsibly and sustainably.

Moreover, by bridging the financial inclusion gap, PMMY contributes to India’s broader development goals, including poverty alleviation, rural development, and women’s empowerment.

Success Stories: Real-Life Impact of PMMY

Across India, countless entrepreneurs have benefited from PMMY loans:

- A street vendor in Rajasthan used a Shishu loan to start a small food cart, eventually expanding into a chain of stalls.

- A small textile unit in Gujarat leveraged a Kishore loan to purchase modern weaving machines, doubling production capacity.

- A micro-manufacturing business in Tamil Nadu secured a Tarun loan, opening a second factory and creating jobs for dozens of workers.

- An established artisan cooperative in Uttar Pradesh utilized a TarunPlus loan to modernize operations and export handicrafts internationally.

These stories underscore PMMY’s role in transforming small ideas into thriving businesses that contribute to both local and national economies.

Pradhan Mantri MUDRA Yojana (PMMY) empowers India’s micro and small entrepreneurs with loans, schemes, and support. Learn eligibility, benefits, and application process. For official details, visit Mudra official website.

Candidates interested in nursing opportunities can explore the latest openings at HPRCA Assistant Staff Nurse Recruitment 2026.